Does the app approve loans?

No. ShambaBoy App provides verified farm activity data and ShambaScore signals. The lender remains responsible for credit policy, underwriting, and compliance.

Agricultural verification infrastructure for verified farm work.

Financial institutions

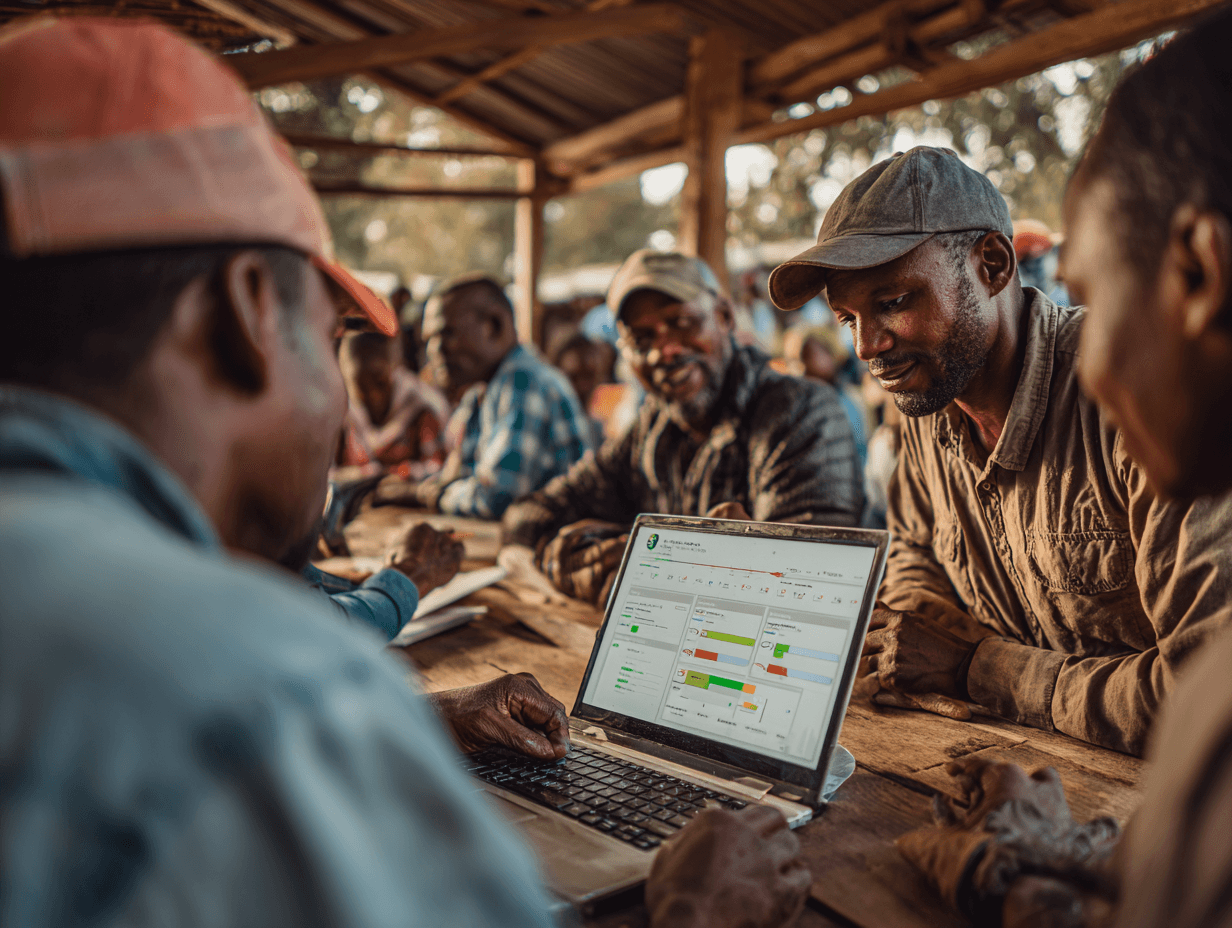

ShambaBoy App turns GPS, photo, timestamp, worker, and approval evidence into ShambaScore signals lenders can review without relying on collateral or self-reported farm income.

ShambaScore runs from 0 to 100 and updates from app-captured field evidence.

Incubating farms can be separated from farms with enough verified operating history.

Partner access can expose score, tier, evidence summary, and last updated date.

ShambaBoy provides verified data signals; lending decisions remain with the lender.

App workflow

01

Supervisors assign field tasks with proof requirements.

02

Workers capture GPS, photos, timestamps, notes, and identity-backed submissions.

03

Approvals and evidence checks roll into ShambaScore and partner-ready summaries.

No. ShambaBoy App provides verified farm activity data and ShambaScore signals. The lender remains responsible for credit policy, underwriting, and compliance.

A farm profile can be self-reported. ShambaScore is built from field evidence captured as work happens.